What Is A Credit Score And How Do You Build A Great One? (part 2)

What Is a Credit Score and How Do You Build a Great One? (Part 2)

Welcome back to Part 2 of our Bank & Loans series! In our first article, we talked about how credit cards aren't a trap at all they're actually one of the most useful financial tools available, as long as you treat them like a debit card and pay your full balance every single month.

But here's the question that trips up a lot of people: why bother using a credit card at all if you're just going to pay it off in full anyway? The answer comes down to one number that will quietly shape almost every major financial decision you make for the rest of your life your credit score.

If you ever plan to buy a house, finance a car, start a business, or even rent an apartment in some cities, you're going to need a solid credit score. Let's break down exactly what it is, why it matters so much, and how you can build one from the ground up.

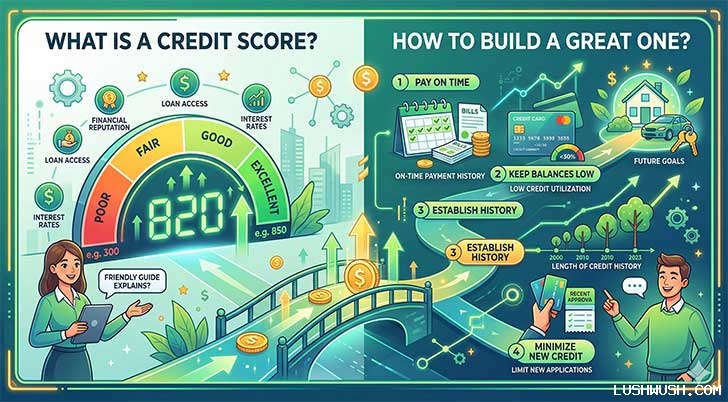

What Is a Credit Score, Really?

Think of your credit score as your "financial report card."

Back in school, your grades told teachers how reliable and consistent you were as a student. In the adult world, your credit score is a three-digit number typically ranging from 300 to 850 that tells banks and lenders how reliable you are with borrowed money.

Here's why that number carries so much weight:

- A low score (say, 550) signals risk. Lenders may reject your loan application outright, or they'll approve you but charge a steep interest rate to offset the risk they're taking on.

- A high score (750+) signals trust. Lenders compete for your business and offer you their best rates, because statistically, you're a safe bet.

Why This Number Is Worth Tens of Thousands of Dollars

This isn't just an abstract concept it has a very real dollar impact. Let's say you're buying a $350,000 house with a 30-year mortgage.

- With a poor credit score (around 620), you might be offered an interest rate of 7.5%. Over 30 years, you'd pay roughly $530,000 in interest alone.

- With an excellent credit score (760+), you might qualify for a rate closer to 6.0%. Over the same 30 years, your total interest drops to around $405,000.

That's a difference of over $125,000 enough to buy a second home in some parts of the country simply because of a few habits you built years earlier. The same logic applies to car loans, personal loans, and even the interest rate on your credit card itself.

The 3 Golden Rules to a Great Credit Score

Building a strong score isn't some hidden secret reserved for finance professionals. The algorithms used by credit bureaus (like FICO and VantageScore) are looking for a handful of very specific, very learnable behaviors. Master these three rules, and your score will climb steadily and predictably.

1. The 100% On-Time Payment Rule

This is, without question, the single most influential factor in your credit score it typically makes up about 35% of the total calculation. Lenders want proof that you pay your bills on the exact day they're due, every time. Even one payment that's 30 days late can knock your score down significantly and stay on your credit report for up to seven years.

The Strategy: Set up autopay through your banking app so your credit card balance is paid in full, three days before the due date. Don't rely on memory or willpower automate it so a late payment becomes structurally impossible.

Example: If your statement balance is $620 and your due date is the 15th, schedule autopay for the 12th. That three-day buffer protects you from processing delays, bank holidays, or app glitches that could otherwise cause an accidental late payment.

2. The 30% Utilization Rule

"Credit utilization" simply measures how much of your available credit you're actively using at any given time. This factor accounts for roughly 30% of your score nearly as important as on-time payments.

Here's a concrete example: if your credit card has a $1,000 limit and your balance is $900, you're sitting at 90% utilization. To a lender, that pattern looks like someone who's financially stretched or leaning too heavily on borrowed money even if you always pay it off.

The Strategy: Aim to keep your utilization under 30% of your total limit at all times.

Example: If your card's limit is $1,000, try to keep your spending under $300 per billing cycle. If you have multiple cards with a combined limit of $10,000, keep your total balances under $3,000. Pay it down, let the lower balance report to the bureaus, and repeat the cycle each month. This single habit shows lenders you're disciplined and not living paycheck to paycheck on credit.

3. The "Don't Close Old Accounts" Rule

A portion of your score about 15% is based on the average age of your credit accounts. The longer your credit history, the more trustworthy you appear, because lenders have more data proving you're consistent over time.

The Strategy: If you open your very first credit card today, plan to keep it open indefinitely. Even years down the road, when you qualify for a flashier card with better travel rewards or cash back, don't close the old one.

Example: Say you opened your first card in 2020 with a $1,500 limit. By 2030, you might barely use it, but keeping it open even just for a $6 coffee purchase once a month, followed by an immediate autopay payoff preserves ten years of positive history. Closing that account would instantly shrink your average credit age, which can cause a noticeable, avoidable dip in your score.

Bonus Factors Worth Knowing

While the three rules above cover the bulk of your score, two smaller factors round out the picture:

- Credit Mix (about 10%): Having a healthy blend of credit types a credit card, a car loan, maybe a student loan shows you can manage different kinds of debt responsibly. You don't need to go out and open new accounts just for variety, but don't be afraid of a mix that occurs naturally over time.

- New Credit Inquiries (about 10%): Every time you apply for new credit, a "hard inquiry" appears on your report and can ding your score slightly for a few months. Applying for five store credit cards in one weekend is a red flag to lenders space out applications and only apply when you genuinely need the credit.

Patience Pays Off

Building a great credit score is a marathon, not a sprint. You will not wake up with a perfect 850 after one month of good behavior credit bureaus want to see sustained patterns over months and years, not a single lucky streak.

But here's the encouraging part: the formula is completely within your control. Pay on time, every time. Keep your balances low relative to your limits. Let your oldest accounts age gracefully. Do those three things consistently, and your score will climb steadily often crossing into "good" territory (670+) within 12 to 18 months, even if you're starting from a thin or damaged credit file.

That rock-solid financial reputation you're building today is what will save you tens of thousands of dollars in interest on the mortgage, car loan, or business loan you take out years from now.

Have you checked your credit score recently? Are you actively working to build it up, or are you dealing with the aftermath of a few missed payments? Let me know in the comments below I'd love to hear where you're starting from.

Curious how much your current interest rate is actually costing you or how much you could save by improving your credit score before your next loan? Run the numbers with our free Smart EMI & Interest Calculator and see exactly how your credit profile translates into real dollars saved or lost over the life of a loan.

All comments, feedback, information or materials except email addresses submitted to Lush Wush shall be considered non-confidential and its property. By submitting such comments, feedback, information or materials to us, you agree to a no-charge assignment of all worldwide rights. For the best interest of the community, please refrain from posting vulgar comments, profanity, or personal attacks. Comments submitted may automatically be flagged for review by our moderation team before appearing on the website.