Good Debt Vs. Bad Debt: When Is It Okay To Borrow Money? (part 3)

Good Debt vs. Bad Debt: When Is It Actually Okay to Borrow Money?

Welcome to the third and final part of our Bank & Loans series. In Part 1, we covered how to use a credit card without ever paying a cent in interest. In Part 2, we walked through how to build a rock-solid credit score from zero. Today we're tackling the topic that makes most people flinch: debt.

A Tale of Two Borrowers

Picture two coworkers, Sarah and Maria, both 29 years old, both earning $58,000 a year, both sitting on the same $30,000 in savings after a work bonus and a few years of disciplined saving.

Sarah decides to reward herself. She puts $30,000 toward a brand-new SUV, financing the remaining $18,000 at 7% interest over five years. It feels amazing driving off the lot.

Maria makes a very different call. She uses her $30,000 as a down payment on a $150,000 rental duplex, financing the rest with a mortgage. It's less exciting than a new car, and honestly, her friends think she's being boring with her money.

Five years later, the difference between these two decisions is not small. It's not even close. We'll walk through the actual math later in this article, because the numbers tell a story that "debt is always bad" simply doesn't capture. Both women borrowed money. Only one of them built wealth doing it.

Why "All Debt Is Bad" Is Outdated Advice

Most of us grew up hearing some version of "if you can't pay cash, you can't afford it." It's well-meaning advice, and for a lot of purchases, it's still correct. But it's also incomplete, and incomplete financial advice can quietly cost you hundreds of thousands of dollars over a lifetime.

Here's the piece that gets left out: banks, corporations, and wealthy individuals borrow money constantly not because they're reckless, but because they understand that debt is a tool, not a moral failing. A hammer isn't "bad" because it can smash a window. It's bad when it's used the wrong way. Debt works the same way.

The entire skill of managing debt well comes down to one distinction: does this loan take money out of your future, or does it put money into it? That's the line between bad debt and good debt, and once you can see it clearly, you'll never look at a loan offer the same way again.

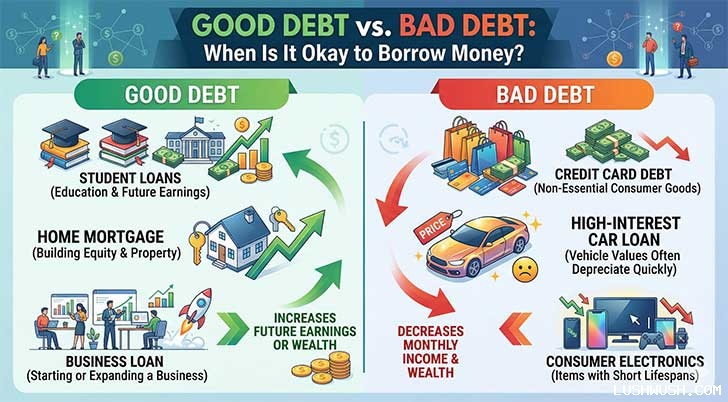

What Is Bad Debt? The Wealth Destroyer

Bad debt is borrowing money to buy something that loses value the moment you own it and produces zero income in return. You're paying interest on a purchase that's actively getting cheaper while you pay it off.

Credit Card Debt on Depreciating Purchases

If you put $4,000 of clothes, electronics, or a vacation on a credit card and only make minimum payments, you're not just spending $4,000. At a typical U.S. average credit card APR of around 24%, paying only 3% minimums, that balance can take over 13 years to clear and cost you more than $3,800 in interest alone nearly doubling the original price of items that were worth far less the day after you bought them.

High-Interest Auto Loans on New Vehicles

A new car loses roughly 20% of its value in the first year and around 60% within five years, according to long-standing industry depreciation data. So if you finance a $40,000 new car at 7% APR over six years, you'll pay close to $8,900 in interest. Meanwhile, the car itself might be worth $16,000 by the time you've paid it off. You've spent nearly $49,000 total on an asset now worth a third of that.

This doesn't mean you should never buy a car on credit most people need a car to get to work, and that's a legitimate need. It means the car itself is not building your wealth. It's a cost of living, not an investment, and it should be treated that way when you're deciding how much to spend and how long to finance it.

The verdict: Bad debt pulls money out of your future every single month and leaves you with an asset worth less than what you paid. It should be minimized or avoided entirely whenever possible.

What Is Good Debt? The Wealth-Building Tool

Good debt is borrowed money used to acquire something that either grows in value over time or generates income that covers and ideally exceeds the cost of the loan itself.

Mortgages and Real Estate Leverage

Say you buy a $150,000 rental property with a $30,000 down payment and a $120,000 mortgage at 7% over 30 years. Your monthly mortgage payment (principal, interest, taxes, and insurance combined) lands around $1,050. If you rent the property for $1,400 a month, you're covering the mortgage and pocketing roughly $350 a month in cash flow before other expenses like maintenance and vacancy which a careful investor typically budgets around $200-250 a month for. Even after those costs, your tenant is largely paying down your loan for you, and if the property appreciates at a conservative 3.5% annually, that $150,000 property is worth roughly $178,000 in five years.

Business Loans and Education as Investments

Imagine you want to build a niche content website or a small app that could realistically generate $800 a month in ad revenue within a year, but you need $5,000 to hire a designer and developer. A small business loan at 10% APR over two years costs you around $540 in total interest. If your project hits even half of its revenue goal, you've recovered your entire loan cost within two months of launch.

The same logic applies to education. A $15,000 loan for a certification that moves your salary from $45,000 to $65,000 a year pays for itself in well under a year of the higher income assuming the job market for that credential is real and you've done the research, which is a big assumption worth double-checking before signing anything.

The verdict: Good debt puts more money back into your life than it takes out. It's a tool that compresses years of saving into a single, calculated decision.

Good Debt vs. Bad Debt: Side-by-Side Comparison

Numbers make this distinction much easier to see than definitions alone. Here's how common types of debt actually stack up:

Rental Property Mortgage

- Typical interest rate: 6.5% 7.5%

- Does the asset gain value? Usually, over the long term

- Does it generate income? Yes rental income

- General verdict: Good debt

Primary Home Mortgage

- Typical interest rate: 6% 7%

- Does the asset gain value? Usually, over the long term

- Does it generate income? No (unless rented out later)

- General verdict: Good debt (situational)

Federal Student Loan (in-demand field)

- Typical interest rate: 5% 8%

- Does the asset gain value? N/A it invests in your earning power

- Does it generate income? Yes higher salary potential

- General verdict: Good debt (if ROI is researched)

Small Business Loan

- Typical interest rate: 8% 13%

- Does the asset gain value? Depends on the business

- Does it generate income? Yes if the plan is solid

- General verdict: Good debt (conditional)

New Car Loan (non-essential upgrade)

- Typical interest rate: 6% 9%

- Does the asset gain value? No depreciates fast

- Does it generate income? No

- General verdict: Bad debt

Credit Card Balance (carried monthly)

- Typical interest rate: 20% 29%

- Does the asset gain value? No

- Does it generate income? No

- General verdict: Bad debt

Payday / Cash Advance Loan

- Typical interest rate: 300%+ APR

- Does the asset gain value? No

- Does it generate income? No

- General verdict: Very bad debt avoid

Notice the pattern: it's not really the size of the debt that determines whether it's good or bad a $300,000 mortgage can be excellent debt, while a $3,000 credit card balance can quietly wreck your finances. What matters is what the money is buying and whether that purchase pays you back.

The Golden Question Before You Borrow

Before you sign any loan agreement or swipe a card for a large purchase, ask yourself one question:

"Will this purchase make me money or increase in value over time?"

If the honest answer is no, it doesn't mean you can never buy the thing it just means you should pay cash for it, or wait until you can. If the answer is yes, and you've actually run the numbers rather than just hoping for the best, borrowing might genuinely be your smartest move.

A useful gut-check: if you wouldn't borrow money to buy the exact same asset from a stranger with no marketing or excitement attached, be honest with yourself about why you're considering it now.

Common Mistakes People Make With "Good Debt" (What NOT to Do)

Calling something "good debt" doesn't automatically make it safe. Here are the mistakes that trip up even well-intentioned borrowers.

- Buying too much house. A mortgage is good debt, but a $500,000 mortgage on a $70,000 salary can still sink you, regardless of appreciation potential. Lenders may approve you for more than you can comfortably afford.

- Ignoring vacancy and repair costs on rental property. A property that only breaks even when it's 100% occupied isn't a safe investment one bad tenant or one broken furnace can turn "good debt" into a monthly loss.

- Taking student loans without checking real earning data. A $60,000 loan for a degree with a median starting salary of $32,000 is bad debt wearing a good debt costume. Always check actual salary outcomes for a specific program before borrowing.

- Starting a business loan without a revenue plan. "I have a great idea" is not a repayment plan. Good debt requires a realistic path to income, not just optimism.

- Confusing "tax-deductible" with "profitable." Interest being deductible reduces the cost slightly; it does not make a bad investment good.

- Borrowing for an appreciating asset with no cash cushion. Even the best investment can turn into a crisis if an unexpected expense hits and you have no emergency savings to fall back on while you wait for the asset to pay off.

Real-World Example: The $30,000 Decision

Let's go back to Sarah and Maria from the opening story and actually run their five-year numbers.

Sarah's SUV: She financed $18,000 at 7% APR over five years, paying roughly $3,350 in total interest on top of the $30,000 she paid upfront. Five years in, her SUV (which cost $48,000 all-in when you count the loan) is worth an estimated $19,000 to $21,000 based on typical depreciation curves. Her net position: she spent roughly $51,350 total and holds an asset worth about $20,000. That's a real, permanent loss of over $31,000 in exchange for five years of driving a nice car a completely reasonable trade-off if that's what she valued, but it built her zero wealth.

Maria's duplex: Her $30,000 down payment plus five years of mortgage paydown on the $120,000 loan leaves roughly $107,000 still owed (a 30-year mortgage pays down slowly in the early years). At 3.5% annual appreciation, her $150,000 property is worth close to $178,000. That gives her about $71,000 in home equity. On top of that, she's collected an estimated $300$350 a month in positive cash flow after expenses, or roughly $19,000$21,000 over five years. Her total position: somewhere around $90,000$92,000 in wealth built from an initial $30,000 investment while her tenants covered most of the loan payments along the way.

Same starting amount. Same five years. One friend is $31,000 poorer in net worth; the other is roughly $90,000 richer. That's not a lucky break it's the direct, mathematical result of the good debt vs. bad debt distinction in action. (Real estate values and rental income vary by market and aren't guaranteed these figures are illustrative, not a promise of returns.)

Your Practical Action Plan Before Taking Any Loan

Next time you're considering a loan of any size, run through this checklist before you sign anything:

- Calculate the true total cost. Add up every dollar of interest over the full life of the loan, not just the monthly payment. A loan calculator makes this a 30-second task instead of a guessing game.

- Identify what the money is actually buying. Write it down in one sentence: "This loan buys me [X], which will [gain value / generate income] because [specific reason]."

- Compare the interest rate to the realistic return. If you're borrowing at 9% to invest in something that might return 6% on a good year, the math is already working against you.

- Stress-test the downside. What happens if the tenant moves out, the business is slower than expected, or your income drops for two months? Make sure you can survive the worst realistic case, not just the best one.

- Keep a cash cushion before you leverage up. Good debt works best when you're not one emergency away from default.

- Only borrow the minimum needed to accomplish the goal. More debt isn't automatically more wealth it's more risk with more potential upside, which only makes sense if the fundamentals are sound.

This article is for general educational purposes and isn't personalized financial advice your income, goals, and risk tolerance are unique, so it's worth running your specific numbers past a licensed financial advisor or accountant before committing to a large loan.

Beginner FAQ: Good Debt vs. Bad Debt

Is a car loan always bad debt? Not automatically. A modest, reasonably priced car loan that gets you to a job you couldn't otherwise reach is a practical necessity, not a wealth-building move that's fine. It becomes bad debt specifically when the loan is oversized relative to your income or financed at a high rate for a vehicle that's more luxury than necessity.

Can a mortgage ever be bad debt? Yes. If the monthly payment stretches your budget so thin that you can't save or handle emergencies, or if you're buying at the very top of an overheated market with no plan to stay long enough to ride out a downturn, a mortgage can absolutely become bad debt despite the "real estate always goes up" reputation.

Should I rush to pay off good debt early? Not necessarily. If your mortgage is at 6.5% and you could reasonably expect a similar or higher return by investing extra cash instead, paying it off early isn't automatically the optimal move though there's real value in the peace of mind of being debt-free, which is a legitimate factor even when the math is close.

What credit score do I need to get good terms on good debt? Generally, a score of 700+ opens up meaningfully better mortgage and business loan rates, while scores above 740760 tend to unlock the very best pricing lenders offer. If you haven't built your credit score yet, that's exactly what Part 2 of this series walks through step by step.

Debt isn't the villain we were taught to fear, and it isn't the free lunch some corners of the internet make it sound like either. It's leverage a tool that magnifies whatever decision you make with it. Used on a depreciating want, it magnifies your losses. Used on a genuine, well-researched asset or opportunity, it can compress a decade of saving into a handful of years. The difference isn't luck. It's asking the golden question, running the real numbers, and being honest with yourself about the answer before you sign.

Before you take out any loan, run the real numbers first. Our free Smart EMI & Interest Calculator breaks down your exact monthly payment, total interest paid, and full amortization schedule in seconds so you can see clearly whether a loan is working for you or against you before you commit.

All comments, feedback, information or materials except email addresses submitted to Lush Wush shall be considered non-confidential and its property. By submitting such comments, feedback, information or materials to us, you agree to a no-charge assignment of all worldwide rights. For the best interest of the community, please refrain from posting vulgar comments, profanity, or personal attacks. Comments submitted may automatically be flagged for review by our moderation team before appearing on the website.