Credit Cards For Beginners: How To Use Them Without Getting Into Debt (part 1)

Credit Cards for Beginners: How to Use Them Without Getting Into Debt (Part 1)

Welcome back to our Bank & Loans series. Over the last few weeks, we've walked through how to save consistently, how to budget your income so it actually stretches to the end of the month, and how to start investing in assets that grow over time. Today we're tackling a topic that makes a lot of beginners nervous: credit.

For many people, the words "credit card" sound like a trap. Almost everyone knows someone who got a card, overspent, and spent years digging out of the hole. Those stories are real, and they're the reason so many people swear off credit entirely and stick to cash or debit cards for life.

But here's the thing: a credit card isn't good or evil. It's a tool. A hammer can build a house or smash a thumb, depending on who's holding it and how carefully they swing. A credit card works the same way. Used with a little discipline, it can protect your money, save you cash, and open financial doors. Used carelessly, it can bury you in debt that takes years to climb out of.

Let's break down exactly how to use one safely, with real numbers so you can see precisely what's at stake.

What Is a Credit Card, Actually?

When you swipe a debit card, you're spending money you already have. Your bank checks your account balance, and if it's not there, the transaction gets declined. Simple.

A credit card works differently. You're not spending your money you're borrowing the bank's money for a short window of time, usually 21 to 30 days, interest-free, as long as you pay it back in full when the bill arrives.

Debit vs. Credit: A Side-by-Side Example

Say you have $300 in your checking account and you want to buy a $250 jacket.

- With a debit card: $250 leaves your account immediately. Your balance drops to $50.

- With a credit card: The store gets paid by the bank right away, but your $300 stays untouched in your account. You now owe the bank $250, due at the end of your billing cycle typically three to four weeks later.

That gap between "the bank pays" and "you pay the bank back" is where all the opportunity and all the danger lives.

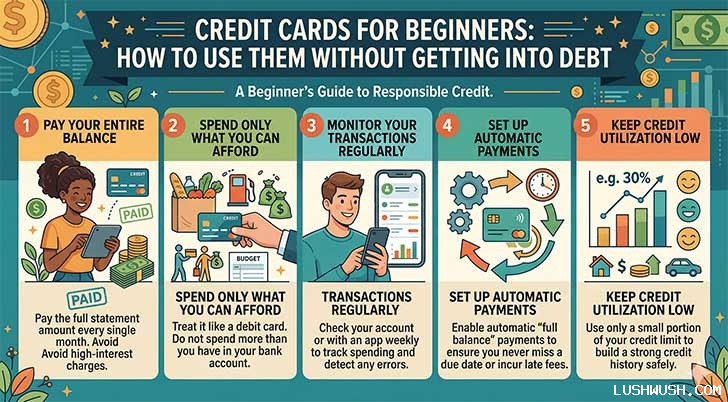

The Golden Rule: Only Spend What You Already Have

The single biggest mistake beginners make is treating a credit card like bonus income instead of a payment method. It isn't extra money. It's a loan with a due date.

The rule is simple: never swipe your credit card for something unless the cash to cover it is already sitting in your bank account right now.

A Real Example: The $500 TV

Let's say you want a $500 TV, but you only have $200 in savings.

- If you put it on a credit card anyway, you're now $300 short when the bill comes due. If you can't cover that gap, the bank starts charging interest often somewhere between 20% and 29.99% APR on the remaining balance.

- If instead you wait, save the extra $300 over the next month, and then buy the TV with cash or with a credit card you can pay off in full you get the exact same television for $500, with zero interest and zero risk.

Follow this one rule consistently, and it becomes mathematically very difficult to fall into a debt spiral. The debt only shows up when you spend money you don't actually have.

How to Avoid Ever Paying Interest

Card issuers make an enormous amount of money from interest charges. But here's the part beginners often don't realize: you can use a credit card for years and never pay a single cent of it, if you understand how the billing cycle works.

Breaking Down Your Statement

At the end of each billing cycle, your card issuer sends a statement with two key numbers:

- The Minimum Payment a small amount, often calculated as roughly 13% of your balance or a flat $25$35, whichever is greater.

- The Statement Balance the full amount you actually spent that cycle.

The minimum payment exists to keep your account "in good standing," not to protect your wallet. It's the number the bank hopes you'll pay, because the unpaid remainder starts accruing interest immediately.

The Real Cost of Paying Only the Minimum

Here's where the math gets uncomfortable. Say you carry a $1,000 balance on a card with a 24.99% APR a fairly typical rate and you only ever pay the $35 minimum each month.

- Month one: you owe roughly $20.80 in interest alone, so only about $14 of your $35 payment actually reduces the balance.

- At that pace, it takes close to 44 months nearly four years to pay off that original $1,000.

- By the time you're done, you'll have paid somewhere around $540 in interest, on top of the $1,000 you originally spent.

That's the trap. A $1,000 purchase quietly becomes a $1,540 purchase, stretched out over almost four years, just because of how the minimum payment is structured.

The solution is just as simple as the trap: pay the full statement balance, not the minimum, before the due date every single month. Do that, and the bank charges you nothing you get an interest-free, 3-to-4-week loan, every cycle, for as long as you use the card.

Why Even Use One, Then?

If you have to pay it back right away anyway, you might be wondering why bother with a credit card instead of just using debit. There are three solid reasons.

1. Fraud Protection

If someone steals your debit card number and drains your account, that's your rent money, your grocery money gone, at least until the bank investigates and (hopefully) refunds you, which can take days or weeks.

If someone steals your credit card number, they're spending the bank's money, not yours. Most major card issuers offer $0 fraud liability, and because it's their funds on the line, they tend to move fast to shut down suspicious activity.

2. Cash Back and Rewards

Most credit cards return a percentage of what you spend, either as cash back or travel points. Say you put $500 a month in ordinary expenses groceries, gas, streaming subscriptions on a card that offers 2% cash back, and you pay it off in full every month.

- $500 12 months = $6,000 in annual spending

- 2% cash back = $120 back in your pocket every year, for purchases you were going to make anyway.

That's not free money exactly it's a rebate on your own regular spending. But it only works in your favor if you're paying the balance off in full. Earn $120 in rewards while paying $540 in interest, and you've lost badly on the trade.

3. Building Your Credit Score

This is arguably the most important long-term reason to use a card responsibly, and it's big enough that we're dedicating our entire next post to it. In short: your credit score affects the interest rate you'll get on a car loan, a mortgage, sometimes even a rental application or job offer. Two of the biggest factors behind that score are payment history (do you pay on time?) and credit utilization (how much of your available credit are you using?).

Common Beginner Mistakes That Sneak Up on You

Even careful people trip over a few predictable pitfalls when they're starting out:

- Running high utilization. If your credit limit is $1,000 and you regularly carry a $600$800 balance, that's 6080% utilization even if you eventually pay it off. High utilization can quietly ding your credit score, independent of whether you ever pay interest. Many experts suggest staying under 30% utilization, and ideally under 10% for the healthiest scores.

- Missing the due date, not the amount. Some beginners have the cash to pay in full but simply forget the date. A single late payment can trigger a fee and sometimes a penalty APR. Setting up autopay for at least the minimum while still manually paying the full balance is a simple safety net.

- Opening cards purely for sign-up bonuses. A $200 bonus sounds great, but if it tempts you to overspend to hit the bonus threshold, or you forget about the card and miss a payment, the "free" bonus can cost far more than it's worth.

A Simple Monthly Framework You Can Copy

Here's a practical way to put all of this together. Imagine your monthly expenses look like this: $250 groceries, $150 gas, $100 subscriptions and utilities, and $500 in other routine spending $1,000 total, all of which you'd be paying anyway with debit or cash.

- Put all $1,000 on a cash-back credit card instead.

- Track it in your budgeting app exactly like you would debit spending the money is still "spent" the moment you swipe.

- When the statement arrives, pay the full balance, not the minimum, before the due date.

- At 2% cash back, you've just earned $20 that month $240 a year for spending money you were always going to spend.

- Meanwhile, your on-time, low-utilization payment history is quietly building your credit score in the background.

Zero interest, zero risk, modest reward, and long-term credit benefits all from one small change in habit.

Key Takeaways

- A credit card is borrowed money, not extra income treat every swipe like it's coming straight out of your bank account.

- Pay the full statement balance, not the minimum, and you'll never pay a cent of interest.

- Only paying the minimum on a $1,000 balance at a typical 24.99% APR can take nearly four years and cost roughly $540 in interest.

- Used responsibly, a credit card offers fraud protection, cash-back rewards, and a path to a stronger credit score.

- Keep your utilization low ideally under 30% of your limit, and under 10% if you're aiming for an excellent score.

Coming Up in Part 2

Now that you understand how to use a credit card without falling into debt, our next post dives into the part everyone asks about: how your credit score is actually calculated, why it matters more than most people realize, and the specific habits that build it fastest.

A quick note: this post is for general educational purposes and reflects common card terms and typical rates your specific card's APR, minimum payment formula, and rewards structure may vary, so always check your own issuer's terms. This isn't personalized financial advice; if you're dealing with existing debt or a major financial decision, it's worth talking to a licensed financial advisor or credit counselor.

Do you currently use a credit card for your everyday expenses, or do you prefer sticking to cash or debit? Let us know in the comments below.a

All comments, feedback, information or materials except email addresses submitted to Lush Wush shall be considered non-confidential and its property. By submitting such comments, feedback, information or materials to us, you agree to a no-charge assignment of all worldwide rights. For the best interest of the community, please refrain from posting vulgar comments, profanity, or personal attacks. Comments submitted may automatically be flagged for review by our moderation team before appearing on the website.