Smart Emi And Interest Calculator Reveal The True Cost Of Your Loan

Smart EMI & Interest Calculator: Find Out What Your Loan Really Costs

You're sitting across from a loan officer. They smile and show you a number: "$500 per month." It sounds reasonable. Affordable. So you sign the papers and walk out feeling good about your decision to finally buy that house or car or start that business.

Then six months later, you look at your loan statement and realize something: you've paid $3,000 and barely made a dent in what you owe. Most of that money went to the bank, not toward actually owning the thing you borrowed for.

This is the loan trap almost everyone falls into. We focus on one numberthe monthly paymentwhen we should be asking a much bigger question: "How much extra am I actually paying for this loan?"

The Real Cost of a Loan Goes Way Beyond the Monthly Payment

Here's what banks don't want you to think about: when you take a loan, you're not just borrowing money. You're renting it. And like any rental, there's a feeexcept this fee can be absolutely massive.

Let's say you borrow $200,000 to buy a home at 8% interest over 20 years. Your monthly payment might be around $1,800. Sounds okay, right?

But here's the shocking part: by the time you finish paying off that loan, you'll have paid nearly $432,000 total. That means you paid $232,000 in pure interest. You paid $1.16 for every dollar you borrowed.

That extra $232,000? That's what banks make. That's what you need to understand before signing anything.

Why Your Monthly EMI Hides the Truth

EMI stands for Equated Monthly Installment. It's the fixed amount you pay every month, but here's the trick: not all of it goes toward actually paying down your debt.

When you make a payment, it's split into two parts:

Part 1: Interest This goes straight to the bank as their profit.

Part 2: Principal This actually reduces what you owe.

And guess what? In the early years of a loan, most of your payment goes to interest. If you're paying $1,800 a month on that home loan, maybe $1,200 goes to interest and only $600 goes toward actually owning the house.

It's not until years later that the balance flips. This is why people who pay off loans early save so much moneythey skip all those interest-heavy early years.

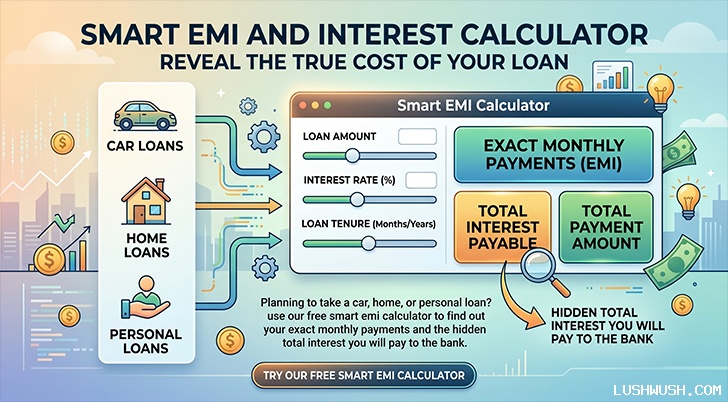

Actually See What Your Loan Costs (Before You Sign)

This is where our calculator comes in. It's not just a toolit's an eye-opener.

Instead of guessing or trusting what the bank tells you, you can see the actual breakdown in seconds. Put in three numbers:

- How much you want to borrow

- The interest rate the bank is charging

- How long you want to take to pay it back

And boomyou see the real picture. Not just the monthly payment. The actual total cost.

The Visual Part Actually Matters

The best part of the calculator? The colored bar at the bottom.

See the blue section? That's the actual money you're borrowingyour principal.See the red section? That's pure interest. That's the extra money walking out of your pocket into the bank's.

When the red section is bigger than the blue section, it's a wake-up call. It means you're paying more in interest than you borrowed in the first place.

And here's where it gets useful: try adjusting the loan duration. See how the red section shrinks when you choose to pay off the loan a year earlier? That's real money you could save.

Three Things You Can Actually Do to Pay Less Interest

Shorten How Long You Take to Pay It Back

Yes, a longer loan means a smaller monthly payment. A 7-year car loan looks better on paper than a 3-year loan. But you're going to pay significantly more in interest over that extra time.

The sweet spot? Choose the shortest timeline you can actually afford without breaking your budget. Even a year or two shorter can save thousands.

Make Extra Payments When You Can

This is the secret nobody talks about. Whenever you get a bonus, a tax refund, or extra cash, throw it at the principalnot the interest.

When you reduce the principal, the bank has less money to charge interest on going forward. It's like breaking the cycle early. One extra $5,000 payment in year 2 might save you $20,000 in total interest by the time the loan is done.

Always Ask for a "Reducing Balance" Rate

Banks sometimes offer "flat rate" interest, which sounds good but is actually a trap. With a flat rate, you pay interest on the original full amount for the entire loan, even as you're paying it down.

A "reducing balance" rate means you only pay interest on what you still owe. This is always better. Always ask for this.

Before You Sign, Run the Numbers

Too many people take loans without actually understanding what they're paying for. They see a monthly number, it seems fine, and they sign.

Don't be that person.

Before you commit to anythinga home, a car, a business loanspend 30 seconds plugging in the numbers. See the real cost. See where the money is actually going.

Use the Smart EMI & Interest Calculator Now

It's free, it's quick, and it might save you tens of thousands of dollars.

The Real Talk: Loans aren't evil. Sometimes borrowing money is the smartest decision you can make. But only if you go in with your eyes open, knowing exactly what you're paying and why. Use the calculator. Make an informed choice. Then borrow with confidence.

All comments, feedback, information or materials except email addresses submitted to Lush Wush shall be considered non-confidential and its property. By submitting such comments, feedback, information or materials to us, you agree to a no-charge assignment of all worldwide rights. For the best interest of the community, please refrain from posting vulgar comments, profanity, or personal attacks. Comments submitted may automatically be flagged for review by our moderation team before appearing on the website.